Advertisement

Inside Ruto’s Ksh5T Infrastructure Fund as World Bank warns of surging poverty levels

Sunday 12th July, 2026 12:06 AM|

President William Ruto’s ambitious Ksh5 trillion National Infrastructure Fund (NIF), billed as a game-changing vehicle for financing Kenya’s infrastructure without piling on new debt, will not resolve the country’s underlying fiscal challenges, the World Bank has warned.

In its latest Kenya Economic Update released on Thursday, July 9, 2026, the Bretton Woods institution said the newly established fund could unlock billions of shillings for commercially viable infrastructure projects but would do little to address persistent weaknesses in revenue collection, public spending efficiency and rising fiscal pressures that continue to weigh on the economy.

The warning comes as the World Bank projects that between one million and 2.4 million additional Kenyans could fall below the poverty line by the end of 2026, driven by rising fuel, food and transport costs linked to global economic shocks.

The lender’s assessment places one of the Kenya Kwanza administration’s flagship economic projects under fresh scrutiny at a time when the government is racing to accelerate growth, create jobs and shield households from mounting cost-of-living pressures.

You Might Also Like

The NIF is central to Ruto’s strategy of financing mega projects without relying heavily on external borrowing. However, the World Bank argues that infrastructure financing alone cannot fix Kenya’s deeper fiscal weaknesses, which it says require sustained reforms in tax administration, public spending and governance.

Ruto’s Ksh5 trillion infrastructure bet

Established under the National Infrastructure Fund Act, 2026, the fund seeks to mobilise up to Ksh5 trillion from pension funds, insurance firms, development finance institutions and other private investors to finance strategic national projects.

Among the projects expected to benefit from the fund are the extension of the Standard Gauge Railway (SGR) to Malaba and the modernisation of Jomo Kenyatta International Airport.

Unlike traditional government borrowing, the fund is designed to attract private capital into infrastructure projects that can generate commercial returns, reducing pressure on public debt.

President Ruto has repeatedly defended the initiative as a cornerstone of his administration’s long-term economic transformation agenda.

Speaking at State House earlier this year, the President said the government would leverage domestic savings and international development financing to deliver critical infrastructure while avoiding excessive external borrowing.

To capitalise the fund, the government has already embarked on the partial privatisation of several state-owned enterprises. The World Bank noted that Kenya raised Ksh106 billion through the sale of a 65 per cent stake in Kenya Pipeline Company (KPC) while a planned reduction of the state’s shareholding in Safaricom is expected to generate approximately Ksh244 billion more for national development priorities.

The proceeds from such transactions are expected to be channelled through the National Infrastructure Fund to finance infrastructure investments.

However, the World Bank cautioned that while these measures could provide an alternative source of infrastructure financing, they would not solve the structural problems at the heart of Kenya’s fiscal challenges.

“Privatisation efforts and asset sales are expected to fund commercially viable infrastructure projects through a new National Infrastructure Fund. However, this would not address the underlying structural weaknesses in revenue mobilisation and spending efficiency, underscoring the need for sustained fiscal consolidation and reforms,” the World Bank said.

The lender further warned that privatisation proceeds are expected to provide only limited fiscal relief because most of the funds raised will be directed towards infrastructure investments rather than addressing budget deficits or reducing debt obligations.

World Bank Flags fiscal risks and rising poverty

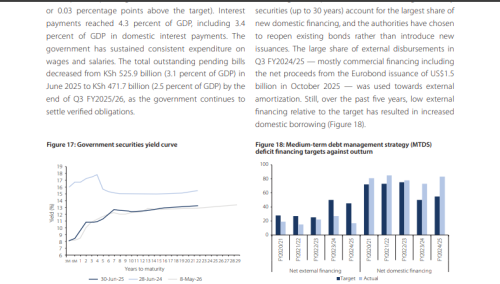

The World Bank‘s concerns stem from Kenya’s deteriorating fiscal position, characterised by repeated revenue shortfalls, spending pressures and increasing dependence on domestic borrowing.

According to the report, total revenue and grants reached 12.1 per cent of GDP in the third quarter of the 2025/26 financial year, falling short of the government’s target of 12.8 per cent. Income tax and Value Added Tax collections recorded the largest underperformance, while expenditure exceeded projections due to higher pension obligations, operational costs and increased development spending.

The lender warned that continued fiscal slippages were undermining policy credibility and weakening the country’s overall fiscal position.

At the same time, external shocks have compounded economic pressures.

The World Bank said the ongoing conflict in the Middle East has disrupted global energy markets, pushing up fuel prices and increasing the cost of transporting goods and services across Kenya.

Food inflation remained elevated at 8.6 per cent in June, while transport costs rose by 9.8 per cent year-on-year, squeezing household incomes and increasing the risk of poverty, particularly in urban areas.

Speaking during the report’s release, World Bank Lead Economist Tom Bundervoet warned that the prolonged effects of the conflict could significantly reverse Kenya’s gains in poverty reduction.

“This conflict could push the poverty rate in Kenya by a certain number of percentage points, which then leads to one million or two million more Kenyans below the poverty line in absolute numbers,” Bundervoet said.

The World Bank estimates that the poverty rate could rise by between two and 4.5 percentage points by the end of 2026, potentially pushing up to 2.4 million more Kenyans below the international poverty line.

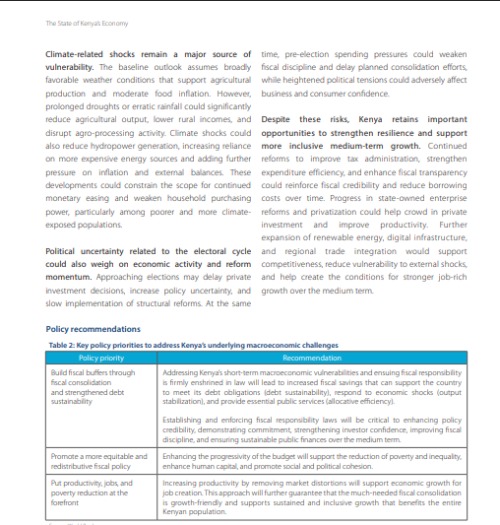

Beyond rising prices, the lender identified climate-related shocks, persistent fiscal vulnerabilities and growing political uncertainty ahead of the 2027 General Election as additional risks that could weigh on economic performance and investor confidence.

The report also lowered Kenya’s economic growth forecast to 4.3 per cent in 2026 and 4.4 per cent in 2027, citing the impact of higher fuel prices, weaker investment growth and pressure on household purchasing power.

To cushion the country against worsening economic conditions, the World Bank called for faster job creation, stronger governance reforms and a more business-friendly environment to encourage private sector expansion.

The warning came a day after Treasury Cabinet Secretary John Mbadi appointed six members to the NIF Board, marking a major step towards operationalising one of President Ruto’s most ambitious economic projects.

While acknowledging the fund’s potential to mobilise private capital for critical infrastructure, the World Bank maintained that Kenya’s long-term economic stability will depend less on asset sales and privatisation proceeds and more on deeper reforms aimed at strengthening revenue collection, improving public spending efficiency and restoring fiscal discipline.

Author

Latest News

Advertisement

More on Inside Politics