Advertisement

Pan-African law firm Bowmans warns Finance Bill 2026 risks raising costs

Tuesday 05th May, 2026 06:25 PM|

Pan-African law firm Bowmans has raised concerns over several proposals in Kenya’s Finance Bill 2026, warning that measures including a shorter tax filing window, new taxes on digital transactions, and higher rental levies could increase costs for businesses and consumers.

In a statement on Tuesday, May 5, 2026, the firm cautioned that the provisions could create double taxation, undermine investment, and lead to mass non-compliance.

Bowmans reviewed the draft Bill, which the government has not yet tabled in the National Assembly. The firm notes that the Bill introduces wide changes to income tax, value-added tax, excise duty, and tax administration rules. While the government wants to expand the tax base, Bowmans says some proposals will make the system more complex and costly.

New taxes on digital payments

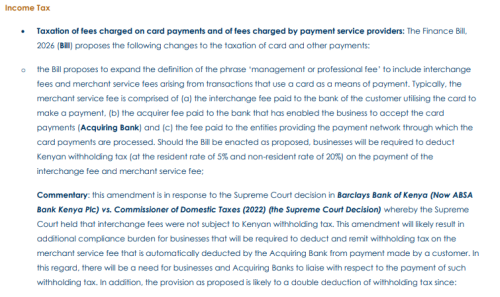

The Bill expands the definition of “management or professional fee” to cover interchange fees and merchant service fees on card transactions. Businesses must deduct withholding tax at 5 per cent for residents and 20 per cent for non-residents on these fees.

You Might Also Like

“This amendment will likely result in additional compliance burden for businesses that will be required to deduct and remit withholding tax on the merchant service fee that is automatically deducted by the Acquiring Bank from payment made by a customer,” Bowmans states.

The firm adds that businesses and acquiring banks will need to liaise on the tax. This coordination may prove difficult in practice.

The review warns of double taxation. The provision as proposed is likely to be a double deduction of withholding tax since: Businesses will deduct withholding tax on the entire merchant service fee that is paid to an Acquiring Bank, and which will typically include the interchange fee; and Acquiring Banks will also be required to deduct Kenyan withholding tax on the interchange fee paid to the issuing bank.

Bowmans explains that businesses often do not know the exact breakdown of the merchant service fee, so they cannot easily avoid the overlap.

The Bill also expands the definition of royalties. It now includes payments to payment network service providers for the use of networks, processing systems, switching systems, clearing systems, and settlement systems. Non-residents will face 20 per cent withholding tax on these payments.

This change reverses a Supreme Court ruling that excluded such payments from royalty treatment. Bowmans notes that experts have previously warned these taxes will raise the cost of card and digital payment channels.

VAT changes hit digital finance

The Bill removes VAT exemption for several digital financial services. Money transfer services, payment processing, settlement services, merchant acquisition, payment gateways, and aggregation services supplied over software or platforms will now attract 16 per cent VAT.

“The proposal would exclude digital players providing financial services from the remit of the VAT exemption,” Bowmans says.

It warns that the change will make fintech players less competitive than traditional banks and will discourage investment in digital payment solutions by increasing costs.

Rental income and capital gains

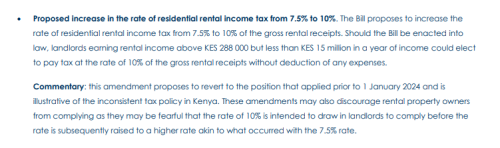

Bowmans highlights the proposed rise in residential rental income tax from 7.5 per cent to 10 per cent of gross rental receipts. Landlords earning between KES 288,000 and KES 15 million a year can opt for this rate without deducting expenses.

The firm says this move shows inconsistent tax policy.

These amendments may also discourage rental property owners from complying as they may be fearful that the rate of 10 per cent is intended to draw in landlords to comply before the rate is subsequently raised to a higher rate akin to what occurred with the 7.5 per cent rate.

On capital gains tax, the Bill expands the tax to cover indirect transfers of shares by non-residents where the shares derive value from Kenya, result in a change of group membership of a Kenyan company, or affect ownership of Kenyan property.

Bowmans warns that the wording is unclear. It questions what “derive their value from Kenya” means – for example, whether a 1 per cent Kenyan value triggers tax on the full gain. The firm also says the terms “group membership” and changes in ownership of Kenyan property lack clear definitions. These gaps, it says, are likely to lead to disputes.

Stricter tax administration

The Bill shortens the deadline for filing income tax returns to the last day of the fourth month after the year-end. Nil returns must be filed within one month. Bowmans points out that this cuts two months from the current timeline and will force companies to deploy more resources, raising compliance costs.

The firm also criticises the removal of weekend and public holiday exclusions when counting days for objections and appeals. Timelines will now run on calendar days, giving taxpayers less time to prepare.

Bowmans raises strong concerns about expanded KRA powers. The Bill allows the authority to issue agency notices to banks and other third parties even when a taxpayer has appealed to the Tax Appeals Tribunal or the courts. This removes a key protection.

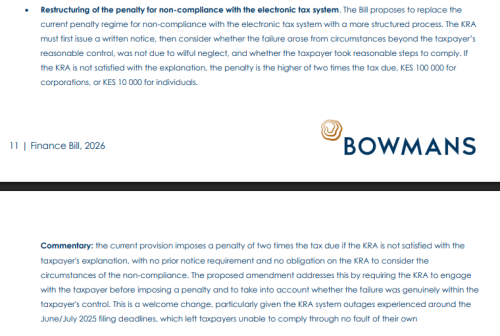

On penalties for electronic tax system failures, Bowmans welcomes the new requirement for KRA to issue a notice and consider factors beyond the taxpayer’s control. However, it notes that penalties can still reach twice the tax due if the authority rejects the explanation.

The Bill also introduces annual reporting obligations for virtual asset service providers. They must submit details of users and transactions to KRA. Bowmans says this aligns Kenya with international standards but adds another compliance layer for crypto platforms.

Other notable proposals

Bowmans flags several other changes. It criticises the plan to deem at least 60 per cent of undistributed profits as distributed by private companies, calling it retrogressive. The firm says businesses often retain earnings for operations or expansion and should not face forced distributions.

It also objects to the removal of the reduced 5 per cent withholding tax on dividends paid to East African Community citizens. This will push the rate to 15 per cent and discourage regional investment.

On the positive side, Bowmans supports clarifications on trust taxation, exemptions for property transfers to REITs, and some electronic system penalty reforms.

Bowmans also flags the new regime for the importation and sale of clothing and worn articles. The Bill deems taxable profit at 5 per cent of the customs value of the imported goods. Traders must pay this tax before customs release the goods, and it is a final tax.

“This amendment is intended to widen the scope of tax compliance by introducing a mechanism for the taxation of a traditional ‘hard to tax’ sector. However, the implementation of this provision is likely to raise questions as to its fairness since it requires that the traders pay income tax on a deemed profit even before the goods are cleared,” the firm says.

Bowmans concludes that while the Bill aims to raise revenue and modernise the tax system, many proposals will increase the cost of doing business. The firm warns of higher costs in fintech, digital payments, property, and general compliance.

It says unclear rules on capital gains and the risk of double taxation could hurt investor confidence.The review stresses that frequent policy changes create uncertainty. Bowmans urges policymakers to balance revenue needs with predictability and ease of doing business to protect economic growth.

The National Treasury had assured Parliament that the 2026 Finance Bill will not introduce new taxes or raise existing tax rates, in a move aimed at calming public concern over tax policy and stabilising the economy.

Treasury Cabinet Secretary John Mbadi told the National Assembly Committee on Budget and Appropriation that the government will instead focus on widening the tax base and improving compliance through automation within the Kenya Revenue Authority (KRA), rather than increasing tax burdens on current taxpayers.

He said lessons from past protests over tax proposals have informed a more cautious approach, while also noting that reforms in revenue collection remain necessary to improve efficiency.

Author

Kenneth Mwenda

Kenneth Mwenda is a business, sports, and politics digital writer with over seven years of experience in journalism, covering breaking news, feature stories, and in-depth analysis across a range of beats.

For inquiries, he can be reached at [email protected]

View all posts by Kenneth MwendaLatest News

Advertisement

More on Business