Advertisement

Why Kenya’s loan defaults will stay high in 2026

Monday 17th November, 2025 04:41 PM|

Kenya’s banking sector will continue to struggle with high loan defaults in 2026, mainly because the government still owes large sums to contractors and service providers. This is the key message from a new report by Fitch Ratings, which warns that unpaid public-sector bills remain the biggest threat to banks’ asset quality.

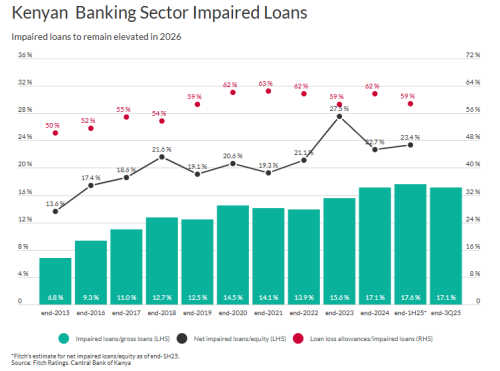

Fitch notes that the impaired loans ratio has climbed sharply over the past decade. It rose from 6.8 per cent in 2015 to 17.6 per cent by mid-2025. The agency says the spike is closely linked to delayed government payments, which have pushed many businesses and suppliers into financial distress.

Between mid-2005 and mid-2022, public-sector arrears reached Ksh664 billion. Most of this amount was owed to state corporations. The government has not provided clear updates on the arrears accumulated after that period.

The long delays have weakened borrowers’ ability to repay loans, a situation made worse by the economic effects of the pandemic, a volatile exchange rate, and high inflation.

You Might Also Like

High interest rates in recent years have also reduced credit demand, while banks preferred to invest in government securities that offered better returns. As a result, loan growth was extremely weak-only 1 per cent in 2024 and another 1 per cent in the first half of 2025 after adjusting for exchange-rate movements.

The slow growth pushed the overall impaired loans ratio higher because existing problem loans were not offset by new, healthier lending.

There has been a small improvement. The impaired loans ratio eased slightly to 17.1 per cent by August 2025. Fitch attributes this mild change to the return of loan growth.

The Central Bank of Kenya began reducing the base lending rate in August 2024 as inflation eased. By late 2025, the rate had been cut by 375 basis points to 9.25 per cent. Lower interest rates should support more borrowing and improve the repayment capacity of customers with floating-rate loans.

Pending bills slow recovery

Fitch forecasts stronger loan growth in the second half of 2025, with further improvement in 2026. It expects mid-single-digit growth this year and double-digit growth next year.

This will help reduce the impaired loans ratio, although only modestly. According to the agency, the ratio will not fall sharply until the government clears a significant share of its arrears.

The government has tried to address the problem. In September 2023, it formed a pending bills verification committee to check the legitimacy of the outstanding amounts.

The committee has verified 86 per cent of the Ksh664 billion claims and recommended that some arrears be paid using money from future privatisation deals. However, Fitch says public-sector arrears are still likely to stay high in the short term despite these efforts.

Even so, the agency believes banks are strong enough to absorb losses. The sector’s loan loss allowance covered 59 per cent of impaired loans by mid-2025. Net impaired loans-after deducting provisions-were equal to 23 per cent of the sector’s total equity.

Fitch says risk to capital remains manageable because banks generate strong pre-impairment operating profit, equivalent to 9 per cent of average gross loans in the first half of 2025. This profit gives banks a cushion to withstand higher loan losses and still grow their capital.

Among the four Kenyan banks rated by Fitch, KCB had the highest impaired loans ratio at 21.3 per cent at mid-2025. NCBA followed with 13.2 per cent, I&M Bank with 12.9 per cent, and Stanbic Bank Kenya with 9.5 per cent.

All four banks recorded pre-impairment operating profits of between 8 and 10 per cent of average loans, which Fitch says is strong enough to handle potential shocks.

Overall, the agency’s assessment is clear: Kenya’s loan default problem will persist into 2026 unless the government makes faster progress in settling what it owes. Lower interest rates and a more stable economy will help, but resolving pending bills remains the key to easing pressure on banks.

Author

Kenneth Mwenda

Kenneth Mwenda is a business, sports, and politics digital writer with over seven years of experience in journalism, covering breaking news, feature stories, and in-depth analysis across a range of beats.

For inquiries, he can be reached at [email protected]

View all posts by Kenneth MwendaLatest News

Advertisement

More on Insights