Advertisement

Why rising inflation is forcing banks to push for rate hike

Monday 08th June, 2026 11:03 AM|

Banks in Kenya are shifting their attention towards Treasury bills and calling for higher interest rates as uncertainty builds ahead of the Central Bank of Kenya (CBK) Monetary Policy Committee (MPC) meeting on June 9, 2026.

The Kenya Bankers Association (KBA) has taken a clear position: inflation risks are rising, and monetary policy must respond. In its Research Note No. 3 of 2026, the KBA argues that a rate hike would help anchor inflation expectations and stabilise prices.

“A timely upward adjustment of the Central Bank Rate will effectively anchor inflation expectations and support price stability in the medium term,” it states.

The timing matters. Inflation has climbed again, driven mainly by fuel costs. Headline inflation rose to 6.7 per cent in May 2026, up from 4.4 per cent in March. The increase follows a sharp rise in global oil prices linked to supply disruptions in the Middle East. Higher transport and production costs have fed into the local economy, pushing up prices beyond fuel alone.

You Might Also Like

For bankers, this environment changes how risk is priced. Lending becomes less predictable when inflation is rising, and the direction is uncertain. That is one reason banks are increasing demand for short-term government paper such as Treasury bills. These instruments offer safer returns while policy direction remains unclear.

The shift is visible in recent CBK auctions where demand for T-bills has remained strong, with bids exceeding available securities. This behaviour reflects a cautious banking sector that prefers guaranteed government returns over higher-risk private sector lending during periods of uncertainty.

At the same time, the KBA is pressing the CBK to raise the Central Bank Rate from its current level of 8.75 per cent. The argument is rooted in inflation control. According to the report, inflation pressure is not only coming from fuel but also from second-round effects across transport, manufacturing and food supply chains.

The note explains, “inflationary pressures have re-emerged from oil supply shock, triggering expectations of higher price rises from the shock’s second-round effects.”

Weak growth, rising inflation

This concern is not limited to prices alone. Economic growth has also slowed. Kenya’s GDP growth eased to 4.6 per cent in 2025, down from 5.7 per cent in 2023. Forecasts suggest a further slowdown to around 4.5 per cent in 2026. High-frequency indicators, including the Purchasing Managers’ Index, show weak business activity, with firms reporting reduced orders due to higher costs.

This combination of slower growth and higher inflation creates a difficult policy environment. It limits how aggressively the CBK can act, but it also increases pressure to maintain credibility on inflation control.

Credit conditions add another layer of caution. Private sector credit grew by 8.1 per cent in March 2026 after earlier reductions in the policy rate. Lending rates eased to around 14.7 per cent, but non-performing loans remain high at 15.6 per cent. This signals strain in repayment capacity. If inflation continues to rise, borrowers could face further pressure, increasing default risks for banks.

This is another reason banks are favouring Treasury bills. Government securities reduce exposure to credit risk while still offering attractive yields in a high-rate environment. It is a defensive move rather than an expansion strategy.

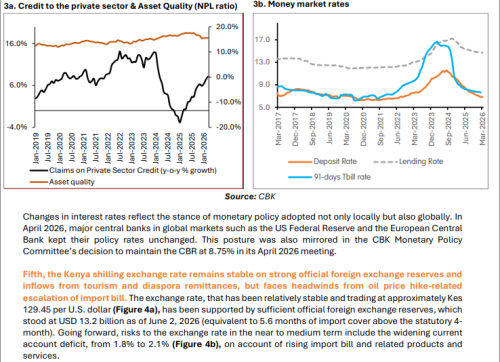

External pressures also matter. The Kenya shilling has remained relatively stable at about Ksh129 to the US dollar, supported by foreign exchange reserves of around $13.2 billion. However, rising oil import costs are widening the current account deficit, increasing future vulnerability.

The KBA notes that while credit growth is recovering, uncertainty around future interest rates is holding back stronger lending activity. Banks are therefore balancing two risks: the risk of lending too aggressively in an uncertain economy, and the risk of missing returns from safer government instruments.

The broader policy question facing the CBK MPC is whether to raise rates to contain inflation or hold steady to support growth. The KBA clearly leans towards tightening. It argues that inflation expectations must be anchored early to prevent further price spirals.

For markets, the focus is now on the June 9 MPC decision. Any adjustment to the Central Bank Rate will influence lending rates, Treasury yields, and banking sector behaviour in the months ahead.

What is already clear is that banks are positioning defensively. Rising inflation, weaker growth signals, and uncertain policy direction have pushed them towards Treasury bills and away from longer-term lending. The outcome of the MPC meeting will determine whether this trend strengthens or reverses in the second half of 2026.

Author

Kenneth Mwenda

Kenneth Mwenda is a business, sports, and politics digital writer with over seven years of experience in journalism, covering breaking news, feature stories, and in-depth analysis across a range of beats.

For inquiries, he can be reached at [email protected]

View all posts by Kenneth MwendaLatest News

Advertisement

More on Business