Kenya’s long-term insurance sector hits Ksh110.4B, up 17 per cent – IRA

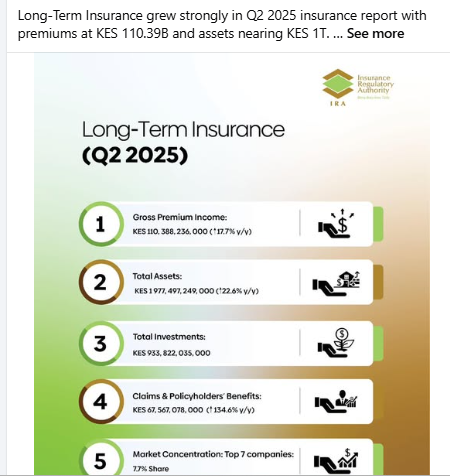

By Kenneth Mwenda, September 25, 2025Kenya’s long-term insurance sector showed strong growth in the second quarter of 2025. According to the latest report from the Insurance Regulatory Authority (IRA), posted on their Facebook account on Thursday, September 25, 2025, gross premium income reached Ksh110.4 billion, representing a 17.7 per cent increase compared to the same period last year.

“Long-Term Insurance grew strongly in Q2 2025 insurance report with premiums at KES 110.39B,” the post read.

This growth highlights rising demand for long-term insurance products, including life and retirement policies.

Total assets in the sector increased to Ksh1.98 trillion, up 22.6 per cent from Q2 2024.

This reflects steady expansion as insurers strengthen their financial base while managing day-to-day operations. Total investments also grew, reaching Ksh933.8 billion. Insurers continue to place funds in various investment channels, ensuring they can meet policy obligations and maintain financial stability.

Claims and policyholder benefits rose to Ksh67.6 billion, driven mainly by higher payouts on life insurance and group life policies. While premiums are growing, rising claims underscore the need for careful management to maintain sector profitability.

Growth amid low penetration

The market remains somewhat concentrated, with the top seven companies controlling a small but significant portion of total market share. This indicates that while a few major players dominate certain segments, smaller insurers are working to expand their footprint in underserved areas.

Industry experts note that long-term insurance penetration in Kenya is still low relative to the population. However, the sector benefits from growing awareness of the importance of financial protection. With life expectancy rising and more Kenyans planning for retirement, demand for long-term insurance is expected to continue increasing.

The sector also benefits from strong investment income. Returns from government securities and other investment instruments provide additional revenue streams, helping insurers manage claims and maintain solvency.

At the same time, rising management expenses and commissions to intermediaries can affect overall net earnings, highlighting the need for effective cost management.