Advertisement

CBK boss Thugge: Kenya’s banking sector remains stable and resilient

Wednesday 10th June, 2026 01:11 PM|

Central Bank of Kenya (CBK) Governor Kamau Thugge has said Kenya’s banking sector remains stable and resilient, citing strong capital buffers, high liquidity levels and a decline in non-performing loans despite prevailing economic uncertainties.

Speaking during the release of the latest Monetary Policy Committee (MPC) statement on Wednesday, June 10, 2026, Thugge said key indicators show that the country’s banking industry continues to maintain strong capital and liquidity positions while remaining profitable.

“The banking sector remains stable and resilient,” Thugge stated.

He noted that capital adequacy and liquidity ratios have consistently remained above the minimum statutory requirements, underscoring the sector’s ability to withstand potential economic shocks.

You Might Also Like

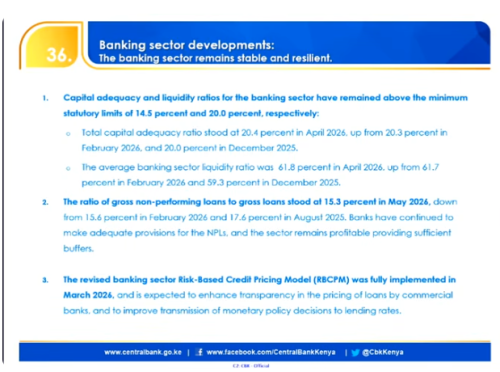

According to CBK data, the total capital adequacy ratio stood at 20.4 per cent in April 2026, up from 20.3 per cent in February and 20.0 per cent in December 2025. The ratio remains well above the statutory minimum requirement of 14.5 per cent.

Strong liquidity levels

The governor also pointed to improved liquidity across the banking sector, saying banks continue to maintain sufficient cash reserves to meet their obligations.

The average banking sector liquidity ratio rose to 61.8 per cent in April 2026, compared to 61.7 per cent in February and 59.3 per cent in December 2025.

“The average banking sector liquidity ratio was 61.8 per cent in April 2026 up from 61.7 per cent in February 2026 and 59.3 per cent in December 2025,”Thugge said.

The figure is significantly higher than the statutory minimum requirement of 20 per cent.

Bad loans decline

Thugge further revealed that the level of non-performing loans (NPLs) has continued to decline, signalling improving credit quality within the sector.

The ratio of gross non-performing loans to gross loans stood at 15.3 per cent in May 2026, down from 15.6 per cent in February and 17.6 per cent in August 2025.

“Banks have continued to make adequate provisions for the non-performing loans, and the sector remains profitable, providing sufficient buffers,” he said.

Transparency in loan pricing

The CBK governor also highlighted the full implementation of the revised Risk-Based Credit Pricing Model (RBCPM) in March 2026.

He said the framework is expected to improve transparency in loan pricing by commercial banks and strengthen the transmission of monetary policy decisions to lending rates.

The latest assessment comes as the CBK seeks to support economic growth while safeguarding financial sector stability, with the banking industry remaining a key pillar of the country’s economy.

Author

Latest News

Advertisement

More on Business