World Bank explains why lower Kenya interest rates do not guarantee economic growth

By Aloys Michael, July 14, 2026Lower Kenya interest rates are often seen as a catalyst for faster economic growth. The logic appears straightforward: cheaper borrowing should encourage businesses to take loans, invest, expand operations and create jobs.

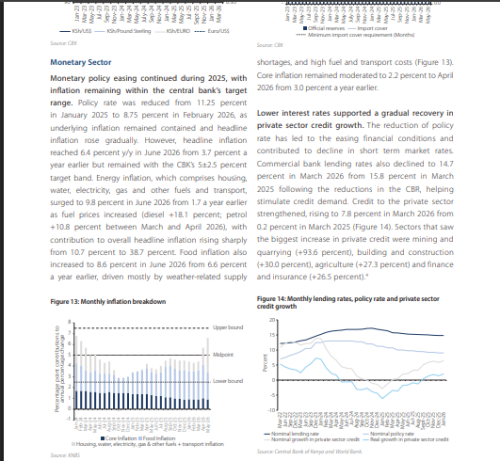

But according to the latest World Bank Kenya Economic Update, the relationship is far more complex. While falling interest rates can support economic activity, they do not automatically translate into higher borrowing, stronger investment or faster growth. The report offers a clear answer to a question frequently asked by businesses and investors: If rates are falling, why aren’t companies borrowing more?

The World Bank says lower borrowing costs are only one factor influencing business decisions. Companies also consider demand for their products, operating costs, economic uncertainty and future profitability before taking on new debt. As a result, even when the Central Bank of Kenya lowers rates, businesses may remain cautious if broader economic conditions remain challenging.

“Domestic macroeconomic conditions remain broadly supportive of growth,” the World Bank states, pointing to easing inflation, lower interest rates and improving private sector credit Kenya has recorded in recent months. However, the institution also warns that external shocks and domestic fiscal pressures continue to weigh on business confidence.

One of the biggest challenges highlighted in the report is the economic impact of conflict in the Middle East. The crisis has increased global fuel prices, raising production, transport and operating costs for businesses across Kenya. Higher costs can discourage investment even when the lending rates Kenya borrowers face are declining.

“The conflict in the Middle East weighed on Kenya’s macroeconomic performance through multiple transmission channels,” the report notes. According to the World Bank, these channels include higher energy costs, inflationary pressures and broader economic uncertainty that can affect investment decisions.

The report suggests that businesses borrow when they see profitable opportunities, not simply because loans become cheaper. A manufacturer facing weak demand, rising fuel costs or uncertainty about future market conditions may delay expansion plans despite lower borrowing costs. Similarly, a retailer may postpone opening new outlets if consumer spending remains under pressure.

Another factor is the transmission lag between monetary policy and economic activity. When the Central Bank of Kenya cuts rates, the effects are rarely immediate. Commercial banks may take time to adjust lending practices, while businesses often spend months evaluating investment opportunities before seeking credit. This means the full impact of lower interest rates can take time to filter through the economy.

The World Bank nevertheless expects private sector credit Kenya businesses receive to continue recovering. Lower financing costs, easing inflation and improving macroeconomic stability are expected to support lending and investment over the medium term. The report projects Kenya’s economic growth of 4.3 per cent in 2026 following an estimated 4.6 per cent expansion in 2025, supported partly by improving credit conditions.

However, the institution cautions against assuming that monetary policy alone can drive growth. Public debt remains elevated at 70.2 per cent of GDP, while fiscal pressures and revenue shortfalls continue to constrain economic policy. These factors can influence investor confidence and business sentiment even in a lower-rate environment.