Advertisement

Treasury accepts Ksh25B in oversubscribed 15-year bond switch

Monday 19th January, 2026 10:33 PM|

The Central Bank of Kenya (CBK) has successfully concluded a switch auction for a 15-year Treasury bond, accepting Ksh25.17 billion in bids after strong investor participation, underscoring continued demand for government securities in the domestic market.

The auction involved the exchange of holdings from the maturing T-Bond Issue No. FXD1/2016/010 (ISIN KE5000006329) into the reopened T-Bond Issue No. FXD1/2022/015 (ISIN KE700009329), as part of the government’s ongoing domestic debt management strategy.

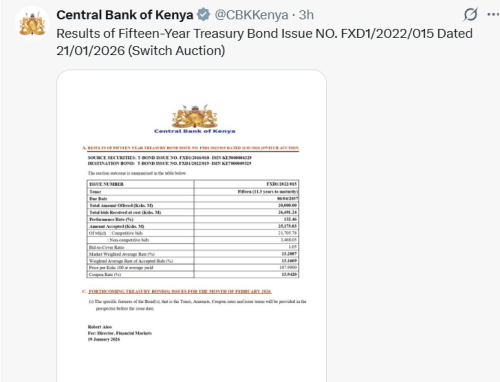

“Results of Fifteen-Year Treasury Bond Issue NO. FXD1/2022/015 Dated 21/01/2026 (Switch Auction),” the CBK X post dated Monday, January 19, 2026, read.

Switch auction records strong demand

The government had offered Ksh20 billion under the switch, but total bids received amounted to Ksh26.491 billion at cost, translating to a performance rate of 132.46 per cent and indicating oversubscription.

You Might Also Like

CBK accepted Ksh25.173 billion, comprising Ksh21.706 billion from competitive bids and Ksh3.468 billion from non-competitive bids. The resulting bid-to-cover ratio stood at 1.05.

The switch was open to investors holding unencumbered positions in the 2016 bond as of January 19, 2026. Eligible investors were allowed to exchange their holdings ahead of the bond’s maturity in August 2026, providing continuity in government securities exposure.

Pricing details from the auction show a market-weighted average rate of 13.2087 per cent, while the weighted average of accepted bids was 13.1669 per cent. The price per Ksh100 at the accepted average yield was 107.9900.

The destination bond carries a coupon rate of 13.9420 per cent and has approximately 11.3 years to maturity, with a final redemption date of April 6, 2037.

Extending maturities and smoothing redemptions

The switch auction serves as a liability management tool for the government, allowing it to extend the maturity profile of domestic debt and smooth future redemptions.

By encouraging investors to move from the 2016 bond into a longer-dated instrument, the Treasury reduces near-term refinancing pressures.

For investors, the operation provides an opportunity to maintain long-term exposure to government securities at prevailing market rates. The original 2016 bond carried a higher coupon of about 15.039 per cent, but its maturity later this year would have exposed investors to reinvestment risk, particularly in an environment where interest rates are expected to ease.

The successful uptake reflects continued appetite among institutional investors for longer-tenor instruments, which offer predictable cash flows and relatively attractive yields in the current market.

The CBK also indicated that additional Treasury bond issues are scheduled for February 2026. Details on the tenor, issue amounts, coupon rates and other terms will be provided in the respective prospectuses ahead of the issue dates.

Author

Latest News

Advertisement

More on Business