Advertisement

KRA sets 8% fringe benefit tax interest rate for July–September 2026

Wednesday 08th July, 2026 06:55 PM|

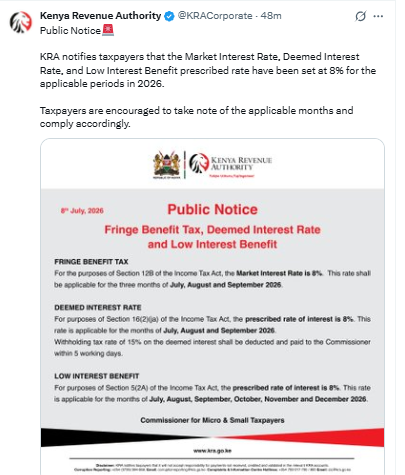

The Kenya Revenue Authority (KRA) has set the market interest rate for Fringe Benefit Tax (FBT) at 8 per cent for the period covering July, August and September 2026, requiring employers to use the prescribed rate when calculating taxable benefits arising from employee loans.

The announcement, contained in a public notice issued on July 8, 2026, also sets the prescribed deemed interest rate at 8 per cent for the same three months, while the low interest benefit rate will remain at 8 per cent from July through December 2026.

“For the purposes of Section 12B of the Income Tax Act, the Market Interest Rate is 8%. This rate shall be applicable for the three months of July, August and September 2026,” KRA said.

The prescribed rate is a key benchmark used by employers, payroll managers and tax professionals when determining Fringe Benefit Tax on employee loans offered at interest rates below the market rate or on interest-free loans. Where the interest charged to an employee is lower than the prescribed rate, the difference may be treated as a taxable employment benefit under Kenya’s Income Tax Act.

You Might Also Like

For employers, the announcement means payroll systems and tax calculations should apply the 8 per cent market interest rate for all qualifying employee loans during the July–September 2026 period. This helps businesses remain compliant with KRA’s tax requirements and avoid errors when filing returns.

Employees who receive staff loans at concessional rates are also affected, although the responsibility for calculating and remitting Fringe Benefit Tax generally rests with the employer. The prescribed rate determines whether a taxable benefit arises from such loans.

KRA also confirmed that the prescribed rate of deemed interest will remain at 8 per cent for July, August and September 2026.

“For purposes of Section 16(2)(ja) of the Income Tax Act, the prescribed rate of interest is 8%. This rate is applicable for the months of July, August and September 2026,” the notice states.

The tax authority further reminded taxpayers that withholding tax at the rate of 15 per cent on deemed interest must be deducted and paid to the Commissioner within five working days. Businesses extending loans or engaging in transactions covered under the deemed interest provisions should therefore continue applying the prescribed 8 per cent rate when calculating their tax obligations.

Prescribes interest rate

KRA also announced that the prescribed interest rate for the low interest benefit will remain at 8 per cent for July, August, September, October, November and December 2026.

“For purposes of Section 5(2A) of the Income Tax Act, the prescribed rate of interest is 8%. This rate is applicable for the months of July, August, September, October, November and December 2026,” the taxman said.

The latest notice provides certainty for employers, accountants, payroll administrators and businesses by confirming the official interest rates applicable during the second half of 2026.

KRA publishes these prescribed rates periodically to guide taxpayers on the calculation of Fringe Benefit Tax, deemed interest and low interest benefits under the Income Tax Act, helping employers meet their tax compliance obligations while ensuring employee loan benefits are taxed correctly.

Author

Latest News

Advertisement

More on Business