Revealed: How Africa’s mineral wealth could boom amid global supply chaos

By Aloys Michael, May 2, 2026As global commodity markets face geopolitical shocks and supply chain tightening, Africa’s mineral-rich regions could emerge as key beneficiaries, driven by rising demand for critical minerals and industrial raw materials worldwide.

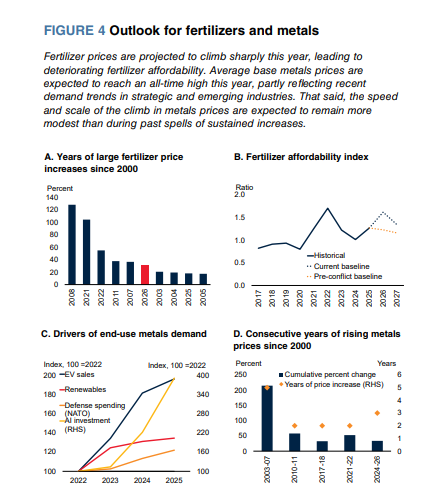

According to the World Bank’s Commodity Markets Outlook (April 2026), base metals and minerals are entering a new era of structural strength, with prices projected to climb 17 per cent in 2026, driven by steadily growing demand amid increased production costs and persistent supply tightness.

The report adds that base metals such as aluminium, copper, and tin are expected to hit all-time highs, underpinned by demand from renewable energy, broader electrification technologies, and data centres.

In other words, the global transition to clean energy, electric mobility, and artificial intelligence is colliding with constrained supply, creating a structural boom for critical minerals.

For Africa, and particularly East Africa, the implications are profound.

The World Bank notes that metals markets are being tightened not only by demand but also by “inelastic short-term production and a raft of supply challenges,” including geopolitical disruptions and export constraints.

This mismatch between surging demand and constrained supply has placed resource-rich developing regions in a strategic position.

East Africa sits on the margins of several critical mineral belts. Kenya has deposits of titanium, rare earth elements, limestone, and soda ash, while neighbouring Democratic Republic of Congo (DRC) dominates global cobalt supply, and Zambia is a major copper producer. South Sudan and Uganda are also expanding extractive industries.

The World Bank’s outlook suggests that these resources are becoming more valuable in a world where supply chains are increasingly fragile and politically exposed.

Kenya’s industrial gamble?

In Nairobi, policymakers are already attempting to reposition Kenya as more than just a raw materials exporter.

At the Kenya Mining Investment Conference and Expo, President William Ruto unveiled an ambitious regional industrialisation vision that could reshape the way East Africa handles its natural wealth.

“We have made the decision that we are going to do this together,” Ruto said, referring to a coordinated plan between Kenya, Uganda, Tanzania, and South Sudan to develop shared industrial infrastructure. “We must use [our resources] to industrialise our countries. We cannot continue to export raw materials.”

The proposal includes a regional oil refinery project, with Ruto signalling Kenya’s willingness to invest up to Ksh500 billion alongside neighbouring states.

The move comes amid parallel private-sector interest. Nigerian industrialist Aliko Dangote has announced plans to build a refinery in Tanzania’s Tanga region, urging East African governments to support large-scale downstream investment.

If realised, these projects signal a shift from export-led extraction to regional value addition,a model long advocated but rarely achieved in Africa’s resource sectors.

However, despite the optimism, the World Bank cautions that the current metals boom is not without risks.

“Supply growth remains constrained, and policy distortions, export restrictions, and localised disruptions could further tighten markets,” the report notes.

This creates a paradox: Africa may be sitting on rising-value assets, but without infrastructure, refining capacity, and regulatory stability, much of the upside could still be captured abroad.

The continent’s history offers a cautionary tale. Previous commodity booms, from oil to cobalt, have often delivered windfalls for foreign investors while leaving limited domestic industrial transformation.

The regional race for minerals

The scramble for critical minerals is already reshaping regional geopolitics. DRC remains central to global cobalt supply chains, while Zambia is attracting renewed copper investment. Tanzania is positioning itself as a refining hub, and Uganda has advanced plans for oil production in Hoima.

Kenya, meanwhile, is attempting to pivot from a services-led economy toward industrialisation anchored in minerals and energy.

But competition is intensifying. Countries are racing not just to extract resources, but to control processing, refining, and export infrastructure, the real sources of long-term value.

“Metals demand is being structurally supported by emerging industries including renewable energy and data centres,” the World Bank warns.

For East Africa, the question is no longer whether demand exists; it is whether institutions, infrastructure, and policy frameworks can capture it.

Ruto’s regional integration push reflects an attempt to avoid the raw materials trap, where countries export value and import finished goods. But execution remains uncertain, particularly in a region where cross-border industrial coordination has historically been difficult.