Advertisement

Revealed: How fast-growing African economies still miss global wealth

Friday 08th May, 2026 11:27 PM|

Low-income economies are projected to become the fastest-growing in the world over the next five years, yet they will still capture only a tiny share of global wealth creation, exposing what a new World Economic Forum (WEF) report describes as a deepening imbalance in the global economic system.

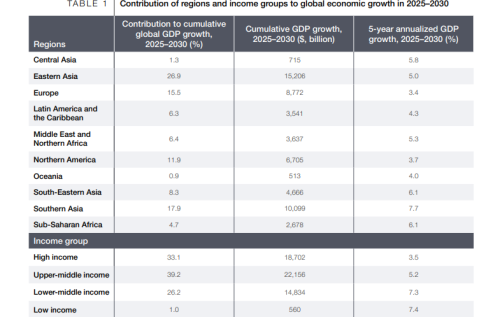

According to the 2026 WEF report, Growth in the New Economy: Towards a Blueprint, low-income countries are expected to grow at an annual average rate of 7.4 per cent between 2025 and 2030, faster than high-income and middle-income economies.

However, despite that rapid growth, they are projected to contribute just 1 per cent of cumulative global GDP growth by 2030.

The findings raise uncomfortable questions about whether fast growth in Africa and other developing regions is translating into real wealth, industrial power and geopolitical influence, or simply reinforcing a global economic structure that keeps poorer countries trapped at the margins.

You Might Also Like

“Old growth strategies in the new economy are unlikely to yield returns as technological disruption, geopolitical fragmentation and mounting debt reshape the foundations of global prosperity,” the report warns.

For African economies, the data represents a troubling paradox: while the continent is home to some of the world’s youngest populations and fastest-growing markets, much of its growth remains concentrated in low-value sectors heavily dependent on raw commodities, consumption and external demand.

Sub-Saharan Africa is projected to record annual growth of 6.1 per cent over the next five years, yet the region will account for only 4.7 per cent of global GDP growth despite its rapidly expanding population.

Kenya, often viewed as East Africa’s economic and technological gateway, reflects many of the opportunities and vulnerabilities identified in the report.

Industrialisation block?

The country has experienced strong growth in digital finance, telecommunications and services, but economists warn that much of Africa’s expansion still lacks the industrial depth needed to generate transformative wealth and high-value exports.

The WEF report identifies information technology services, advanced manufacturing and healthcare as the biggest future drivers of global growth. Yet many African economies remain locked out of these high-productivity sectors because of weak infrastructure, limited financing and technological dependence.

“Technology and knowledge are increasingly central to value creation,” the report states, warning that countries unable to absorb, adapt and apply innovation risk falling further behind in the new economy.

The report also points to major structural barriers facing low-income economies, including inadequate infrastructure, high energy costs and limited access to finance for businesses.

In Sub-Saharan Africa, nearly 89 per cent of countries surveyed identified limited access to finance for business investment as one of the biggest obstacles to growth. More than half also cited expensive energy and inadequate infrastructure as major constraints.

WEF say these weaknesses are preventing African economies from moving beyond commodity exports and low-value consumption-driven growth.

At the same time, rising public debt is tightening fiscal space across many developing countries, limiting governments’ ability to invest in industrialisation, education and technological transformation.

The WEF warns that global public debt is projected to rise to 100 per cent of GDP by 2030, creating new pressure on poorer economies already struggling with high borrowing costs and currency instability.

The report further suggests that the global economy is becoming increasingly concentrated around advanced technologies, strategic industries and geopolitical alliances dominated by wealthier nations.

“Middle-income economies will account for 65 per cent of global growth,” the report says, while Asia alone is expected to contribute more than half of all global expansion by 2030.

For Africa, this raises broader questions about whether current trade systems, debt structures and foreign investment models primarily benefit multinational corporations and external powers rather than local industries.

Economists have long argued that many African countries remain trapped in extractive economic systems where raw materials leave the continent cheaply while finished products and technologies return at far higher costs.

The WEF report warns that “the winners in the new economy will be those who understand competing threats and opportunities and build agile growth pathways.”

For Kenya and the wider African continent, the challenge may no longer be how to achieve rapid growth — but how to finally convert that growth into real ownership of global wealth, innovation and economic power.

Author

Latest News

Advertisement

More on Business