KRA clarifies tax exemption rules on gratuity payments

By Faith Lagat, August 12, 2025The Kenya Revenue Authority (KRA) has issued a public notice clarifying new tax exemption rules on gratuity payments, effective July 1, 2025.

The guidance, anchored in the Finance Act, 2025, represents a major shift in the taxation of retirement benefits and is expected to ease the financial burden on employees and employers.

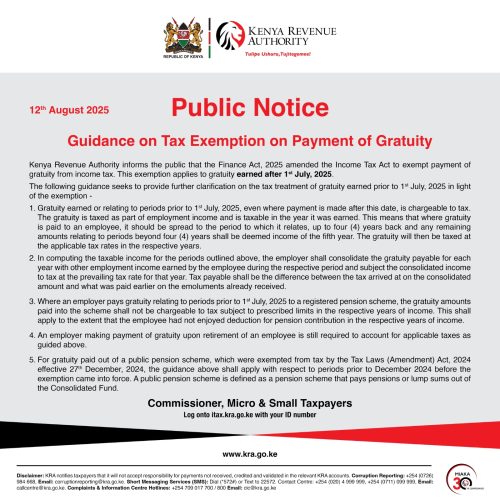

In the notice titled “Guidance on Tax Exemption on Payment of Gratuity” dated August 12, 2025, KRA stated: “Kenya Revenue Authority informs the public that the Finance Act, 2025, amended the Income Tax Act to exempt payment of gratuity from income tax. This exemption applies to gratuity earned after 1st July, 2025.”

The move is expected to particularly benefit public sector workers and employees in formal private sector jobs, where gratuity has traditionally been taxed as a lump sum.

No retroactive application

KRA clarified that the exemption does not apply to gratuity earned before July 1, 2025, even if payment is made after this date. “Gratuity earned or relating to periods prior to 1st July, 2025, even where payment is made after this date, is chargeable to tax. The gratuity is taxed as part of employment income and is taxable in the year it was earned,” read the statement.

For such payments, employers are required to spread the gratuity over the period it was earned, up to four years, with any excess taxed in the fifth year. The amounts must be consolidated with other income and taxed at prevailing rates, with adjustments for taxes already paid. This provision aims to ensure fairness and prevent undue tax burdens on workers receiving delayed payments.

Pension scheme considerations

The notice also addressed gratuity payments made to registered pension schemes. Where an employer channels gratuity relating to periods before July 1, 2025, into a registered pension scheme, the amounts will not be taxed, provided they fall within prescribed limits for the relevant years of income and the employee has not previously claimed deductions.

Additionally, gratuity from public pension schemes—already exempt from December 27, 2024, under the Tax Laws (Amendment) Act, 2024—remains non-taxable, except for portions relating to service before the exemption date, which follow the same tax rules as private schemes.

KRA has urged taxpayers to seek further guidance by visiting itax.kra.go.ke or contacting the authority’s call centre at +254 (020) 4 999 999. While the policy marks a progressive step in retirement benefits taxation, it underscores the need for clear and timely communication to ensure all eligible workers can take full advantage of the new exemptions.