Salasya warns Ksh5T Infrastructure fund could undermine parliamentary oversight

By Mustafa Juma, March 5, 2026Mumias East Member of Parliament (MP) Peter Salasya has raised alarm over the proposed national infrastructure fund, warning that its current structure could weaken parliamentary oversight and undermine constitutional safeguards on public finance.

Taking to his official X account in the wee hours of Thursday, March 5, 2026, Salasya questioned the governance framework of the fund, which is projected to control close to Ksh5 trillion, arguing that concentrating such financial authority under a single cabinet secretary with limited parliamentary supervision poses serious constitutional and accountability concerns.

Parallel financial system

According to the lawmaker, the proposal risks creating what he described as a “parallel financial system” operating outside the full scrutiny of the National Assembly of Kenya.

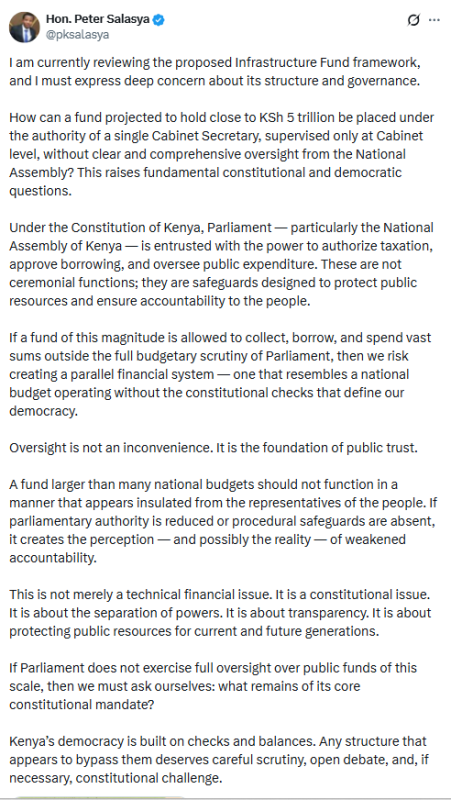

“I am currently reviewing the proposed Infrastructure Fund framework, and I must express deep concern about its structure and governance. How can a fund projected to hold close to KSh 5 trillion be placed under the authority of a single Cabinet Secretary, supervised only at the Cabinet level, without clear and comprehensive oversight from the National Assembly? This raises fundamental constitutional and democratic questions,” Salasya stated.

“Under the Constitution of Kenya, Parliament — particularly the National Assembly of Kenya — is entrusted with the power to authorize taxation, approve borrowing, and oversee public expenditure. These are not ceremonial functions; they are safeguards designed to protect public resources and ensure accountability to the people.”

Oversight

The MP questioned how a fund of such magnitude could be allowed to collect revenue, borrow, and spend large sums without being subjected to the same budgetary oversight that governs other public funds.

He warned that bypassing parliamentary scrutiny could erode public trust and weaken democratic checks and balances enshrined in the Constitution of Kenya.

“If a fund of this magnitude is allowed to collect, borrow, and spend vast sums outside the full budgetary scrutiny of Parliament, then we risk creating a parallel financial system — one that resembles a national budget operating without the constitutional checks that define our democracy,” he added.

Salasya further argued that oversight by elected representatives is a cornerstone of public accountability, particularly when managing resources drawn from taxpayers or public borrowing.

“A fund larger than many national budgets should not function in a manner that appears insulated from the representatives of the people. If parliamentary authority is reduced or procedural safeguards are absent, it creates the perception — and possibly the reality — of weakened accountability,” he stated.

He further framed the issue as more than a financial or technical policy debate, insisting that it touches on constitutional principles such as separation of powers, transparency, and protection of public resources.

He cautioned that if Parliament’s authority over such a massive financial structure is reduced, it could set a dangerous precedent for future public spending arrangements.

“This is not merely a technical financial issue. It is a constitutional issue. It is about the separation of powers. It is about transparency. It is about protecting public resources for current and future generations,” Salasya said.

“If Parliament does not exercise full oversight over public funds of this scale, then we must ask ourselves: what remains of its core constitutional mandate?”

National Infrastructure Fund Bill

Salasya’s remarks come hours after the proposed National Infrastructure Fund Bill, which was introduced on Wednesday, March 4, 2026, continued to attract mixed reactions on the floor of the National Assembly, with critics questioning the heavy influence of the Executive, specifically Treasury Cabinet Secretary John Mbadi, in its management.

Proponents of the bill say it is the surest way for the country to unlock trillions of shillings needed to develop previously neglected areas.

The bill proposes a board of nine directors comprising a chairperson, the Treasury CS or their representative, four independent directors, two persons experienced in senior leadership in development banking, and a chief executive officer.

It provides that the independent directors and the two senior experts shall be recruited competitively through a selection panel created by the Treasury CS.

Once appointed by the CS, the same CS shall determine the directors’ remuneration and sign and review their performance contracts.