Banks push CBK to lower interest rates in upcoming review

By Faith Lagat, October 5, 2025The Kenya Bankers Association (KBA) has called for a cautious reduction of the Central Bank Rate (CBR), citing low inflation, a stable shilling, and the need to stimulate private sector credit growth.

In its bi-monthly Research, released on October 2, 2025, ahead of the Monetary Policy Committee (MPC) meeting scheduled for October 7, the KBA Centre for Research on Financial Markets and Policy highlighted favourable macroeconomic conditions that could support monetary policy easing.

“In view of low inflation and well anchored inflation expectations, and stability in the exchange rate, the need to stimulate credit growth to support economic activity becomes paramount. In this regard, we view that there is scope to further ease monetary policy via a cut in the Central Bank Rate; but laced with caution watching the continuing external vulnerabilities,” states the report.

“Ahead of the MPC meeting on October 7, 2025, the Kenya Bankers Association Centre for Research on Financial Markets and Policy notes in its Research Note released today that there is room for a further reduction in the Central Bank Rate. “

“The Centre observes that, with inflation low and stable, the economy growing at 5.0 per cent in Q2, private sector credit growth still under pressure, and the shilling steady due to strong reserves and remittances, a cautious cut in interest rates could help encourage lending and foster stronger growth.”

Inflation remains within target range

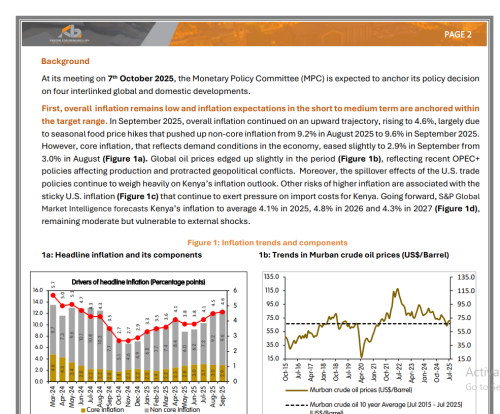

The KBA notes that inflation remains low and stable, creating room for policy adjustment. Overall inflation rose slightly to 4.6 per cent in September 2025, driven by seasonal food price hikes that pushed non-core inflation to 9.6 per cent from 9.2 per cent in August. Core inflation, which reflects demand pressures, eased marginally to 2.9 per cent from 3.0 per cent, remaining within the target range.

“In September 2025, overall inflation continued on an upward trajectory, rising to 4.6 per cent, largely due to seasonal food price hikes that pushed up non-core inflation from 9.2 per cent in August 2025 to 9.6 per cent in September 2025.”

“However, core inflation, which reflects demand conditions in the economy, eased slightly to 2.9 per cent in September from 3.0 per cent in August,” read the report in part.

Forecasts from S&P Global Market Intelligence project inflation at 4.1 per cent in 2025, 4.8 per cent in 2026, and 4.3 per cent in 2027, despite external risks linked to global oil price increases and U.S. trade policies. KBA underscores that this controlled inflation environment provides a foundation for monetary easing.

“Global oil prices edged up slightly in the period (Figure 1b), reflecting recent OPEC+ policies affecting production and protracted geopolitical conflicts. Moreover, the spillover effects of the U.S. trade policies continue to weigh heavily on Kenya’s inflation outlook,” read the KBA report.

“Other risks of higher inflation are associated with the sticky U.S. inflation that continues to exert pressure on import costs for Kenya. Going forward, S&P Global Market Intelligence forecasts Kenya’s inflation to average 4.1 per cent in 2025, 4.8 per cent in 2026 and 4.3 per cent in 2027, remaining moderate but vulnerable to external shocks.”

Modest credit growth

The report points to economic resilience, with Kenya’s economy recording 5.0 per cent growth in the second quarter of 2025. However, it warns of downside risks in the third quarter due to weak demand, against the backdrop of a fragile global economy projected to grow at 2.6 per cent this year.

Private sector credit growth rose modestly to 3.3 per cent in August 2025, marking seven successive months of mild growth after a 2.9 per cent contraction in January. Asset quality remains a concern, with non-performing loans rising to 17.6 per cent by June 2025.

The shilling’s stability, supported by foreign exchange reserves of USD 10.7 billion (4.7 months of import cover) and a 3.91 per cent increase in remittances in August, also strengthens the case for a cautious rate cut. The shilling averaged Ksh129.24–129.26 per USD in September, with medium-term projections showing a gradual depreciation to Ksh133.59 by the end of 2025.

KBA’s analysis suggests that easing monetary policy could encourage lending and support economic growth in line with current economic indicators ahead of the MPC’s decision.