Advertisement

More workers to retire to poverty ‘without a plan’

Friday 18th November, 2022 07:20 AM|

More Kenyans will retire into poverty if the pension system is not reformed quickly to meet their needs.

Experts say it will require an overhaul of the frameworks and must ensure that both formal and informal sectors actively participate in the saving culture, which is considered very low by Kenyan standards.

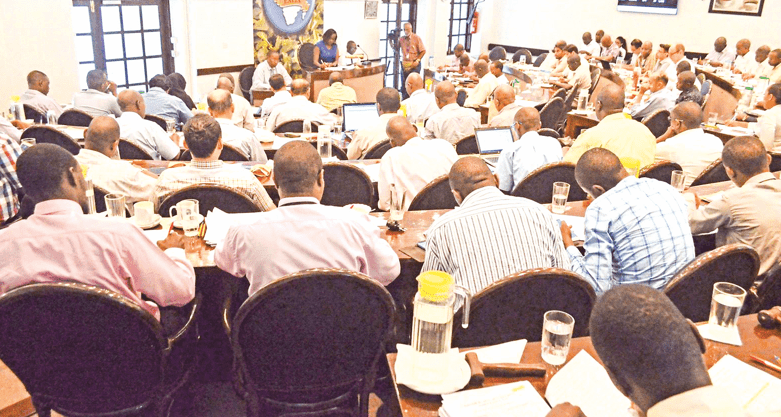

Speaking at the opening of a two-day Pension Trustee Summit by Zamara, former Education CS George Magoha said there was a need for further enhancement and improvement of the retirement benefits framework in Kenya.

He said there should be wider coverage across the working population and, especially, the expansive informal sector which remains excluded from saving for retirement.

Cover basic needs

“Let’s increase the levels of savings in both private and public sectors retirement benefit arrangements to ensure that those covered receive adequate benefits that will cover their basic needs when they retire,” he said.

A recent report by Zamara Kenya Pensions Watch shows that a staggering 83.2 per cent of employed Kenyans in the informal sector have no access to any form of pension savings.

Those concerns were shared by the chief executive of Zamara Investments, Sundeep Raichura, who said the provision of retirement benefits was limited to public sector workers and that the private sector was adequately slow in rolling out pension products tailored to the informal sector.

“Provision of retirement benefits should be a universal basic need and there is a need for further enhancement and improvement of the retirement benefits framework in Kenya to make it more inclusive,” said Raichura.

The Zamara Kenya Pensions Watch 2022 further shows that the median age of the Kenya population is 20.1, but there are 2.2 million Kenyans aged above 60 years, as of 2021, and this figure will nearly triple to 6.3 million Kenyans aged above 60 years by 2040.

Formidable challenge

The expected increase in the ageing population in Kenya presents a formidable social and economic challenge.

It also makes it imperative for the country to put in place a broad and appropriate retirement benefits framework that will ably respond to the challenge by increasing both the quantum of savings as well as the level of coverage for savings in the formal and informal sectors.

“In addition, the public and private sectors need to do their part to ensure that their employees are adequately prepared for retirement,” it reads in part.

Although Kenya’s pension fund sector is ranked the biggest in the region — with over Sh1.4 trillion worth of savings invested in various asset classes — just three million out of 27.1 million people in the labour force have a pension cover.

Cytonn, a real estate and investments company, says despite the significant developments, the pension coverage in Kenya is still low, currently at just 20 per cent. It attributes the slow growth to factors such as market volatility, a slowdown in economic growth, unemployment, and poor access to pension savings before retirement.

Mandatory contributions

Previous attempts have seen Hosea Kili, County Pension Fund (CPF) and the Local Authorities Pensions Trust (Laptrust) chief executive, calling on the sector regulator to consider expanding social security coverage by making pension contributions mandatory for all Kenyans if the sector is to grow.

The establishment of a universal fund, he said, would assist by allocating a percentage of the national budget towards universal pension and medical coverage.

You Might Also Like

Author Profile

Latest News

Advertisement

More on Business